This is a question that many prospective borrowers ask themselves, once they have made the tentative decision to obtain a reverse mortgage: should they work directly with a lender or go through a borrower?

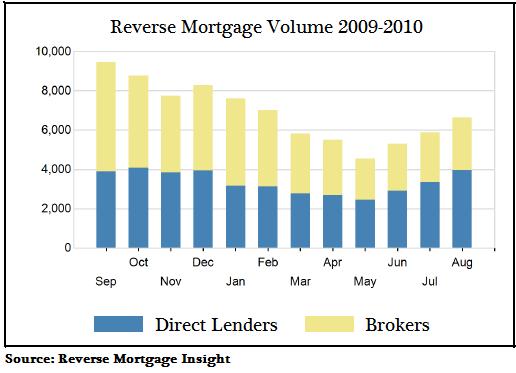

Based on the most recent data, more borrowers are choosing to engage directly with lenders. In August 2010, 60% of reverse mortgages were originated by lenders, compared to only 40% in August in 2009. If you slice the data another way, lenders originated 18% more reverse mortgages – compared to 2009 – while broker loan volume grew by only 6%.

It’s difficult to say for sure what’s driving this trend away from brokers. Their reputation was damaged by the report from the National Consumer Law Center that compared reverse mortgages to subprime mortgages. Brokers were singled out by the report for using unscrupulous practices to enhance their commissions. For example, they have been known to steer reverse mortgage borrowers into inappropriate financial products, such as annuities.

It could also be that changes in reverse mortgage pricing, such as the elimination of origination fees and the service-fee-set-aside (sfsa) and partially subsidized insurance premiums, are making it difficult for brokers to compete, since they can’t offer borrowers such attractive terms. Their lack of competitiveness has been further exacerbated by laws forbidding hidden yield-spread-premiums, which mean that they must earn their commissions directly from the borrower, instead of from the lender.

Since many brokers cannot compete on price, they have taken to selling their expertise and their ability to provide unbiased advice. While there is something to be said for the fact that they don’t have the same financial interest as lenders in originating loans, they still only get paid if elect to obtain a reverse mortgage. In practice, then, they are probably just as biased in lenders when explaining the pros and cons of reverse mortgages.

Finally, given that most lenders offer identical reverse mortgages (that conform to FHA government standards), there probably isn’t much value in advice which purports to help you differentiate one lender from another. In short, the case for using a reverse mortgage broker – as opposed to a direct lender – is looking pretty weak at the moment.

One Response to “Reverse Mortgage Broker or Direct Lender?”

Have Feedback on This Article?

November 9th, 2010 at 4:10 pm

In my view, the primary reason brokers are originating fewer loans has less to do with knowledge, experience, and reputation, and has more to do with sheer numbers. Over the past year, we’ve seen the number of brokers decline steeply due to increased regulations, licensing requirements, and the slumping real estate market where many small brokers simply couldn’t do enough volume to survive. In the past, 7 out of 10 lending companies were brokers, but today it is probably more like 3 out of 10. Interestingly enough, the brokers still collectively do more than 30% of the business, so more folks still “choose” brokers it would seem, but there are just not as many around any more.