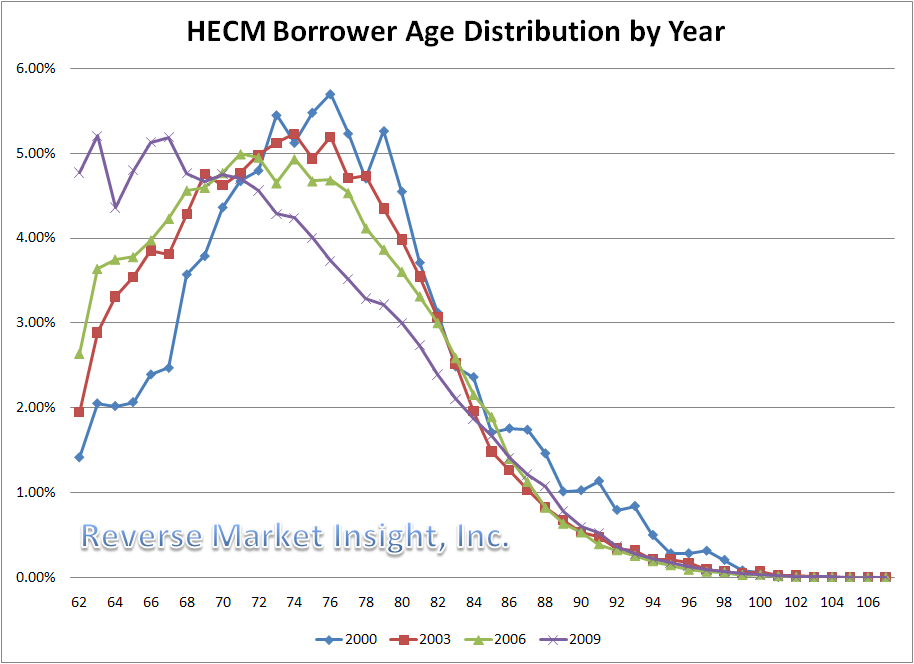

Well, not literally. But the age at which borrowers are obtaining reverse mortgages is steadily falling. According to the most recent industry data, the average age was only 72 in 2009, down from 77 in the year 2000.

This trend is on full display in the chart below, where you can see that the age distribution is gradually being pulled closer, such that the majority of borrowers now hail from the younger side of the eligibility spectrum rather than the midpoint This observation is reinforced by anecdotal evidence, as industry professionals have noticed more and more borrowers in their 60s and fewer in their 70s. Borrowers in their 80s and 90s now represent a smaller proportion of the total than at any point since records starting being kept.

There are a handful of possible explanations for this trend. The first is that relatively younger borrowers are perhaps more comfortable with debt than previous generations. The second is that baby boomers (the first batch of which became eligible for reverse mortgages in 2008) have “higher expectations of living standards.” From a financial point of view, it stands to reason that these borrowers are unprepared for retirement and lack adequate savings. This condition was probably exacerbated by the credit crisis and the subsequent economic recession, which devastated the portfolios of many baby boomers and sent them into early retirement.

While reverse mortgages were previously obtained by borrowers well into retirement, they are now being sought out by those who have only recently become eligible; 30% of borrowers in 2009 were 68 years or younger. It is interesting that such borrowers either don’t have the capacity to simply can’t bear to wait a few more years before obtaining loans. This phenomenon is especially incredible when you consider that borrowing limits are much lower for younger borrowers, who might be better served by waiting 5-10 years after becoming eligible before applying.

While the four lines on this chart show a trend moving entirely in one direction, it’s hard to imagine that it will continue in this way unabated. On the other hand, the explosion of retiring baby boomers should create a tremendous amount of demand among younger borrowers. In addition, the stock market probably won’t return to earlier levels for at least a decade and jobs (especially for the middle-aged) may remain scarce. It will be interesting to see whether this causes the distribution curve to steepen even further.

Have Feedback on This Article?