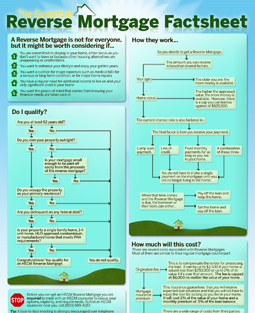

We have recently created a free visual guide for seniors who are looking to understand how reverse mortgages work.

Earlier this week, it was announced that the FHA’s insurance reserves have fallen below the benchmark 2% level of insurance commitments. In fact, it is now only .53%, and some analysts are suggesting that it could soon fall below zero, necessitating a government bailout.

It is not difficult to understand why the FHA’s reserves are falling. You can see from the excellent flowchart below (courtesy of the Wall Street Journal), that in the wake of the housing crisis, the FHA is involved in a growing portion of mortgage lending. In fact, FHA loans now represents nearly 25% of all new mortgages. Moreover, a high proportion of these loans are secured by very little equity- less than 5% in the majority of cases. As a result of the concurrent economic downturn, meanwhile, loans are souring at a faster rate, and the ratio of delinquent 2007 loans has surpassed the percentage of 2004 loans that are delinquent. “Nearly one in five loans it insured in 2007 falls into the category of ‘seriously delinquent,’ ” the agency admitted.

Shaun Donovan, Secretary of the Department of Housing and Urban Development (a Cabinet-level position) has insisted that the agency will remain solvent, and that in fact, its reserves could return the 2% level as soon as fiscal 2012. “In line with many analysts, the agency expects the housing market to turn down again over the next nine months and then to recover. Under this projection, foreclosures would be manageable and the reserves would quickly grow.” Nonetheless, he has delayed the release of the annual FHA audit so that more downside forecasts can be conducted, and included in the report.

Congress isn’t exactly buying this self-declared prognosis. “Rep. Scott Garrett (R., N.J.) introduced a bill last month that would raise minimum down payments to 5%, something that the agency opposes. ‘Others are beginning to see that this could be the next major bailout,’ he said.” Still, the agency is insisting both on its autonomy and its ability to survive this minor crisis unscathed.

It’s unclear how the reverse mortgage program will be affected. The FHA has already lowered the size of maximum allowable mortgages, as a percent of the value of the collateral housing. Shortly thereafter, it paradoxically raised the overall allowable mortgage to $625,000. According to the FHA, “This year, for the first time, we have added an actuarial study of the FHA reverse mortgage, or HECM, program, to the principal study of standard FHA single-family insurance programs supported by the Fund.” Since the report’s release has been delayed, we will have to wait to see whether the reverse mortgage program is in the same dire-financial straits as its conventional mortgage lending program.

Given that home prices have declined so precipitously and that reverse mortgage defaults are also rising, it seems likely that its reserves set aside for reverse mortgage lending are probably proportionately low. At the very least, lending standards will have to be tightened, and perhaps insurance premiums will have to be raised. Naturally, these costs will be passed on to the borrower. If you’re thinking about a reverse mortgage, then, this could be your last chance for a while to get in at good terms.

Over the last couple years, reverse mortgage lending has exploded, such that the product can no longer be considered a niche offering. Now, it looks as if the industry will get another boost, as Wall Street introduces the practice of securitization, which has long since been commonplace in conventional mortgage lending.

For those of you aren’t familiar with this concept, securitization involves the bundling of individual assets (mortgages in this case) into massive portfolios, so that they ca be sold to institutional investors. The idea is that by packaging many mortgages together, the risk declines, since a few defaults will presumably be offset by repayment by the majority of borrowers. By connecting capital markets (i.e. large investors) directly with mortgagers, it is believed that mortgage rates and terms are more attractive than they otherwise would be. (As an aside, it is also believed that securitzation played a large role in the fomenting of the housing bubble and the subsequent financial crisis).

With 110,000 reverse mortgages per year (and rising), Wall Street investment banks have discovered new potential for securitization. In fact, it is surprising that the practice wasn’t introduced earlier, since in some ways, reverse mortgages would seem to constitute the ideal candidate for securitization; due to mandatory FHA mortgage insurance, lenders already bear virtually zero risk in the reverse mortgages they originate. From an investor standpoint, meanwhile, the risk of default is also nil, since taxpayers (via the FHA) are ultimately on the hook for any mortgages that cannot be paid.

On the other hand, there are some inherent differences between reverse mortgages and conventional mortgages, which create a unique investment dynamic. Namely, the time horizon for repayment is typically much longer with a reverse mortgage, and in fact indefinite. Whereas a conventional mortgage borrower must repay the mortgage incrementally over a fixed time period (usually 15 or 30 years), it is impossible to predict when a reverse mortgage will be repaid since it usually only comes due when the borrower dies and/or the home is sold. In addition, whereas a conventional mortgage must be gradually repaid, a reverse mortgage is typically only repaid in full.

It would be difficult for investors, then, to judge how long the mortgage must be held before it will yield a profit. In some ways, then, it is akin to investing in an asset that doesn’t produce a stream of income payments, but only a lump-sum payout at the end of its life. Accordingly, it probably isn’t appropriate for the majority of investors.

How will this affect borrowers? Those with outstanding reverse mortgages won’t be affected in the slightest. For potential borrowers, it could lead to slightly lower interest rates, since a larger supply of capital will presumably drive down prices. Lending standards will probably also be relaxed, since lenders will have virtually zero incentive to ensure repayment. The FHA insurance premium guarantees that investors will ultimately be repaid, regardless of what happens to the value of one’s home (the main variable in a reverse mortgage) in the interim. Once again, it looks like taxpayers will get screwed, but everyone else will come out ahead.

In a new twist, lenders are utilizing reverse mortgages as a substitute – or in some cases, as a compliment to – modifying loans for borrowers having difficulty repaying their loans. The underlying logic is that for many borrowers, including those that have been fortunate enough to receive loan modifications, will still face difficulty repaying their mortgages.

Towards this end, lenders have generally taken one of two approaches. The first involves simply issuing a reverse mortgage for the remaining loan balance, such that the borrower doesn’t have to worry about making additional payments on a mortgage that he can’t afford. Sometimes, the balance of the loan is first reduced, such that the reverse mortgage qualifies for FHA reverse mortgage guidelines. This step is crucial for underwater mortgages, where the borrower’s equity is already negative. Under the second approach, the lender would simply issue a reverse mortgage to the borrower but pocket the proceeds itself. After the borrower passes away, the lender assumes control over the property. Typically, the borrower’s heirs can purchase it back by repaying the reverse mortgage.

Both of these approaches reflect the desperation of lenders, who are are increasingly faced with mortgages that are worth many times the value of the respective homes with which they are associated. Lenders evidently have concluded that selling the properties would involve considerable time and expense, and in many cases would bring in less than what the property was appraised before. Since reverse mortgage are based on appraised value – and not sale value – lenders are able to avoid recognizing the true decline in the property.

If you’re currently having trouble making mortgage payments, and are concerned that even loan modification wouldn’t be enough to forestall foreclosure, this strategy is worth broaching with your lender. Granted, it remains the exception and not the norm, but it doesn’t hurt to ask. In addition, borrowers under the age of 62 are not eligible for FHA-insured reverse mortgages, which could pose a problem from the lender’s standpoint, since a private reverse mortgage carries significant risks. Still, many lenders are eager to avoid foreclosure, because of the legal and financial burden it carries. Accordingly, they may be willing to work with borrowers to develop more creative solutions.

As a result of the gaping hole in its finances, the FHA is currently mulling a new reverse mortgage product: the Mini Home Equity Conversion Mortgage (Mini-HECM). The idea was put forward at a recent real estate conference in San Diego, and since then has been echoing around the blogosphere.

The product is still in the early stages of planning, so it’s unclear exactly how it would function. Basically, it is expected to serve as a more compact and economical version of the existing reverse mortgage product. For borrowers that want to receive cash now in one lump sump payment, the Mini-HECM would presumably allow them to withdraw a smaller portion, though at terms more favorable than existing loans offer. The catch could be that borrowers, then, wouldn’t have the option of withdrawing additional funds later.

In this way, the product would conceivably protect both borrowers and the FHA. Borrowers, while not having the luxury of converting the entire (projected) value of their home into equity, would still be able to withdraw a significant portion, though small enough to ensure that they would have remaining equity that they would receive at the time of sale (and repayment). One of the main criticisms of reverse mortgages is that it encourages borrowers to withdraw all of the equity in their homes, leaving them with little in case of emergency. With the Mini-ECM, borrowers would presumably be prevented from exceeding a certain equity threshold, thereby guaranteeing them an equity reserve that could be tapped in desperate circumstances.

The FHA would also be protected, since the likelihood of default would also decrease. Over the last few years, many reverse mortgages have been pushed underwater (i.e. loan size exceed home value) by the bursting of the housing bubble. This explosion in defaults, however, wasn’t anticipated by the FHA, which insures the majority of reverse mortgages, resulting in an $800 million home in the agency’s finances. It has responded by petitioning Congress for funds and lowering the maximum loan size for all reverse mortgage borrower. The Mini-HECM would provide a further layer of protection.

It seems the government (via HUD and the FHA) are finally getting serious about reverse mortgages. The industry is still something of a free-for-all, lacking comprehensive regulation. With this potential new addition the family of reverse mortgage products, the FHA will hopefully ensure that HECMs are provided in a way that primarily benefits the consumer (rather than the lenders), while also minimizing the exposure of taxpayers.

Demand for reverse mortgages has begun to slacken, due largely to factors beyond the control of (potential) borrowers.

In a nutshell, housing prices remain low, as a result of the economic crisis, and FHA recently issued a new directive that cut the maximum reverse mortgage loan size. Both of these factors strike directly at the heart of reverse mortgages, because they limit the amount of cash available to borrowers. This figure is basically determined by multiplying FHA loan limits (which is expressed as a percentage, and varies by age and in accordance with prevailing interest rates) by the appraised value of one’s home. Since both home values and FHA loan limits are both lower, this translates into a smaller reverse mortgage.

For the majority of reverse mortgage borrowers, this constitutes a serious problem, since many are strapped for cash, and need to withdraw a large percentage of the equity in their home in order to make the loan work. This is especially true for borrowers that have existing liens (i.e. primary mortgages) on their homes, and intend to use the reverse mortgages to repay them.

It’s not clear how long housing prices will remain depressed. The most recent data suggests that a recovery might not be far away, but there are plenty of analysts who think that this represents a “false bottom.” In other words, housing prices could conceivably continue to fall, before ultimately exiting from the downturn. This has important implications for potential reverse mortgage borrowers, since it directly effects the amount of cash they can receive if entering into a reverse mortgage today. Instead, many such borrowers might be inclined to wait until the market recovers before considering a reverse mortgage.

The FHA directive, meanwhile, is probably more permanent. It was enacted both in response to the housing market crash and because of it’s insolvency. Apparently, the possibility of government subsides and/or higher insurance premiums had been considered, but ultimately rejected, in favor of simply lowering maximum loan amounts. As the FHA’s financial problems probably won’t abate, higher loan limits seem unlikely in the near-term.

Then again, if home prices rise, reverse mortgage “defaults” will also subside, and the FHA could contemplate returning the old loan maximums. In this case, reverse mortgage borrowers would be rewarded twice.

With last week’s passage of Assembly Bill 329, California officially became the first state to legislate changes in the reverse mortgage industry. Most other states still lack comprehensive reverse mortgage regulation, such that burden of oversight falls on the Federal Government (via the FHA).

While the law that was ultimately passed represents a watered-down version of the original bill (thanks in no small part to lobbying efforts by the National Reverse Mortgage Lenders Association), and hence doesn’t impose many new restrictions. Namely, it seeks to crack down on “cross-selling” of annuities and insurance products with reverse mortgages, and increase counseling requirements for new borrowers.

The former aim is pretty straightforward. One of the biggest criticisms of reverse mortgages is that they are often paired with annuities by lenders looking to make additional profits. However, since reverse mortgages are inherently structured to give the borrower the option of withdrawing the loan balance in an annual payment, there is little advantage of this annuity. In fact, the California law prohibits lenders from altering the annual payout due to interest rate changes, and imposes steep penalties on those who do. In this, the “annuity option” is preserved.

The counseling requirement, meanwhile, aims to redress the problem that many borrowers were being pressured into reverse mortgages without a thorough understanding of the product’s terms and mechanics. Towards this end, the California law requires lenders to furnish a list of non-profit counseling agencies, so that the borrower can complete a mandatory session prior to obtaining the mortgage. At this counseling session, a written checklist must be signed, that discusses the following topics:

(A) How unexpected medical or other events that cause the prospective borrower to move out of the home, either permanently or for more than one year, earlier than anticipated will impact the total annual loan cost of the mortgage.

(B) The extent to which the prospective borrower’s financial needs would be better met by options other than a reverse mortgage, including, but not limited to, less costly home equity lines of credit, property tax deferral programs, or governmental aid programs.

(C) Whether the prospective borrower intends to use the proceeds of the reverse mortgage to purchase an annuity or other insurance products and the consequences of doing so.

(D) The effect of repayment of the loan on nonborrowing residents of the home after all borrowers have died or permanently left the home.

(E) The prospective borrower’s ability to finance routine or catastrophic home repairs, especially if maintenance is a factor that may determine when the mortgage becomes payable.

(F) The impact that the reverse mortgage may have on the prospective borrower’s tax obligations, eligibility for government assistance programs, and the effect that losing equity in the home will have on the borrower’s estate and heirs.

(G) The ability of the borrower to finance alternative living accommodations, such as assisted living or long-term care nursing home registry, after the borrower’s equity is depleted.

I think last point is particularly important, since reverse mortgages may inadvertently deprive themselves of “outs” in their twilight years. In other words, well many elderly borrowers would like to remain in their homes for the remainder of their lives, we all know that the reality is otherwise. In other words, it’s important for seniors with reverse mortgages to set aside additional cash, as the equity in their homes dwindles to zero over the term of the mortgage.

With this post, I’d like to examine a couple aspects of reverse mortgages that receive little attention in the media, and from lenders: building code violations (and the resulting fines) and tax deductions. The latter is a plus, as it means the true cost of a reverse mortgage is actually lower than the stated cost. The former, however, is is a serious detriment, which could potentially lead to foreclosure.

Neither of these aspects is unique to reverse mortgages. The tax deductibility of mortgage interest is frequently cited by those within the industry as a great benefit, since it means your true cost of interest is lowered by your marginal tax rate. For example, if you pay 35% tax on your income, then the true amount of interest you pay on your mortgage is 35% less than the amount you pay the lender each month, with the difference “subsidized” by the government.

The same applies to reverse mortgages, although conceptually it’s a bit more complicated. That’s because reverse mortgages are often obtained by borrowers that have no intention of directly repaying them. Rather, the expectation is that the borrower’s heirs will handle the repayment after his death. Thus, it’s conceivable that no mortgage interest (or principal for that matter) is paid by the borrower, and hence no tax benefit can be realized.

Still, borrowers ought to be aware that their heirs can deduct the accrued mortgage interest when it ultimately repaid, perhaps after the house is sold. There are also complex estate planning strategies designed to maximize the benefit of the tax deduction. For example, the future heirs may wish to repay a certain amount of interest each year (prior to the loan being repaid) in order to spread the tax deductions over a longer time period of time.

Another option is to use a reverse mortgage to take out a special insurance plan, the proceeds of which will be received upon the death of the borrower. Assuming the insurance policy and reverse mortgage are congruent, this method will effectively turn an asset that would otherwise have been subject to estate taxes and make it un-taxable. Of course, these strategies are extremely complex and it’s recommended that your seek legal counsel, rather than proceed on your own.

The other side of reverse mortgages that I want to explore in this post is the consequence of not maintaining the property that has been mortgaged. Again, just like with conventional mortgages, unpaid property taxes and/or unpaid fines resulting from maintenance violations can result in foreclosure. This is a potentially serious pitfall for seniors that either didn’t have much equity in their properties to begin with, and/or spent the balance of the reverse mortgage too quickly, without setting aside enough cash for maintenance and property taxes.

Reverse mortgage lenders love to point out that there is only one contingency that can result in the property being foreclosed upon. Unfortunately, this is a very serious contingency, especially when you consider that the product is designed for borrowers with precarious financial situations. If your home declines in value and/or the balance of the loan cannot be repaid, it is HUD (via its insurance arm) that is on the hook for the difference. If you don’t keep up with your taxes, or you rack up too many building code violations, the state could put a lien on your home and force an immediate sale of the property. This could leave with very little money for you to put towards a new place to live.

The importance of this consideration cannot be overstated. Make sure that prior to taking out a reverse mortgage that you have enough funds set aside to maintain the property as before. Otherwise, it may make sense to downsize into a more affordable home.

The reverse mortgage industry has exploded over the last decade, growing to 110,000 loans and an estimated 2,700 lenders in 2009. The only way that kind of growth can transpire over such a short time period is with a massive promotional effort, especially when the product in question was considered relatively obscure only last year. Sure enough, reverse mortgage advertisements have permeated the media, and infomercials have flooded late-night TV.

Websites aimed at turning unemployed professionals into successful sellers of reverse mortgages have proliferated, with some using language typically found in “get-rich-quick schemes.” Promises one website, “You really are at the right place at the right time. Not to sound too corny or salesy but this truly is a “GOLDEN OPPORTUNITY” since so few loan officers are working with this niche or have any clue about the secrets to successfully marketing to seniors.” Another advises, “You must never, ever stop marketing. When you take a step back and think about … we really aren’t originators, are we? In reality, we are marketers of our services, and no marketing equals no business.” For anyone on the other end of this transaction, that should set off alarm bells.

For research purposes only, I have spent the last few days watching such commercials and reviewing advertisements. With only a few exceptions, I have been appalled by their inaccuracy. [For the record, I’m not trying to vilify reverse mortgage lenders and loan officers merely for the sake of doing so. I have no truck with those who present the product accurately and market it towards those whose financial circumstances would support obtaining one.]

Unfortunately, the most egregious aspect of reverse mortgage marketing is that lenders present it as a one-size-fits all product appropriate for all retirees. The advertisements often feature happy, older couples enjoying nice meals and luxurious vacations, with the implicit message that “this could be you.” In reality, the product was originally conceived to help those whose financial situations were precarious- hardly a “niche” that would be inclined to use the proceeds for expensive dinners.

For those whose financial situations are already somewhat robust, and simply want a little “play money,” consider that the lending terms of reverse mortgages are somewhat extortionate. This is my second grievance with reverse mortgage commercials: that they gloss over the fees. In reality, upfront fees are substantial, and interest rates are insidiously high, partially as a result of the “yield-spread premiums” which are paid to loan officers for doing little more than standing between you and the lender. They are able to get away with charging these fees because most borrowers don’t know about them and/or don’t understand the way reverse mortgages work. As a result of these costs, you receive only 60% of the value of your home when the loan is obtained, and in exchange, you (or your heirs) forfeit the majority of the proceeds reaped from a sale in the future. As morbid as this sounds, this is fine for those who intend/wish to die in their homes. For those that plan to downsize or move into assisted living facilities in their twilight years, a reverse mortgage could rob you of the funds to do so. Doesn’t sound like a very reasonable trade, does it?

My final point of contention is that reverse mortgage ads ignore the risks, to the point of being misleading. Many ads draw attention to the fact that loans are government insured. While this is true, the insurance is paid by you, but all of the potential benefits inure to the lender. In other words, the insurance is necessary to protect the lender in case you default. Don’t kid yourself into thinking that it benefits you. It’s true that if you stay current on property taxes and maintenance, your loan can’t be foreclosed upon. For those who can’t stay current and/or sell their home for another reason, they may not be left with much equity (if any) after a sale.

Let this be a lesson for those of you eligible to take out a reverse mortgage. Again, that’s not to say that the product isn’t ultimately a reasonable choice for you. Just make sure you take these ads at face value. The fact that reverse mortgages are extremely profitable for lenders means you need to be vigilant.

Based on feedback from our readers, it seems few (potential) reverse mortgage borrowers are aware of the possibility of refinancing a reverse mortgage. The idea of refinancing is typically associated with conventional mortgages, and for good reason! Who would ever think to refinance a loan that they don’t have to repay directly? [Note: I’m not implying that a reverse mortgage doesn’t need to be repaid, but rather that it is often repaid by the borrower’s heirs, after the borrower passes away.]

In many situations, however, it can be extremely beneficial to refinance. The most obvious trigger would be a change in interest rates. Since the balance of a reverse mortgage continues to accumulate interest until it is repaid (as with a conventional mortgage), a lower interest rate would necessarily translate into less interest. For those with fixed rate reverse mortgages, this notion is pretty straightforward.

For those with adjustable-rate mortgages, the math is slightly more complex, and rests on certain assumptions about the direction of short-term variable rates. However, those that took out reverse mortgages many years ago probably were limited to variable-rate products, and might wish to refinance into a fixed-rate loan for peace of mind. As with a conventional mortgage, the savings from lower interest might be offset by fees associated with the refinancing. In the case of reverse mortgages, these can be significant. In other words, unless interest rates drop dramatically (by 2%+), a refinancing probably won’t be economical.

There is another goal of refinancing which is unique to reverse mortgages- increased cash payout. Don’t forget that the initial loan amount was determined largely by factors outside of one’s control: borrower’s age, home value, loan limits, interest rates, etc. In the years since you took a reverse mortgage, you have certainly aged, your house may have appreciated, federally-mandated loan limits may have risen, and/or interest rates may have fallen. All of these trends would entitle you to more cash. This is particularly relevant in the current environment, where home prices are depressed and FHA loan limits are becoming stricter. Refinance five years from now, and there is a good chance that these drawbacks have been alleviated. Not to mention that you are now five years older, which means the lender is actuarially five years closer to being repaid.

The analogy would be to a cash-out refinancing on a conventional mortgage. Again, you must make sure that the increased cash payout more than offsets the fees. One rule of thumb is that the additional cash should exceed fees by two to four times. Consider also that an increased loan size would accrue more interest and possibly erode the value of your remaining equity at an even faster pace.

The latter is an important consideration and could leave your heirs with little if any proceeds after selling your home. It would be even more dire if you were forced to move out, as you could potentially be left with little money to put towards a new home. Thus, even though counseling isn’t usually required with a refinancing, it would probably be beneficial to meet with a professional and be reminded one more time about the potential downsides.