By way of the Consumers Union report (“Examining Faulty Foundations in Today’s Reverse Mortgages”), I recently became aware of a groundbreaking study conducted by the University of Iowa in 2007. The study tested the cognitive decision-making abilities of older persons, and their conclusions strike at the very heart of reverse mortgages.

The researchers behind Orbitofrontal Cortex Real-World Decision Making, and Normal Aging began with the premise that natural aging processes significantly degrade the brain’s prefrontal cortex in a substantial portion of older people. The resulting neural dysfunction, they hypothesized, might explain why many older people engage in faulty decision-making, and appear to be particularly vulnerable to fraud.

The results were startling: “As many as 35 to 40 percent of elders they studied had flawed emotional responses that stem from abnormalities that develop in the brain’s prefrontal cortex. The study also determined that these flaws were leading the seniors to make financial decisions based in part on reward and ambiguity, which follow the same approach used by individuals with acquired prefrontal lesions (traumatic brain injury).” For example, the researchers observed that some of the participants were susceptible to the truth effect, whereby they were more easily persuaded by repeated information, regardless of merit.

Unfortunately, the onset of cognitive decline may coincide with a period of life in which many critical, long-term (financial) decisions need to made, related to “investment of savings and retirement income, purchase of insurance and living trusts, estate planning, and sudden changes in financial roles following the death of a spouse.” As if the constraints posed by limited finances, a lack of income, and general uncertainty about the future weren’t enough, it now turns out that many of these seniors might also lack the proper neurological capacity to make logical decisions on these matters.

If this is the case, then the reverse mortgage system in its current form is probably inadequate. For example, 90% of counseling sessions are conducted over the phone, where there is no way to certify the identity of the borrower, let alone his decision-making capacity. As if that weren’t enough, it seems that that most borrowers treat the counseling session as a mere formality. By the time they are required to complete it, they have already made the decision to obtain a reverse mortgage and are probably far along the process. Finally, due to the truth effect and related phenomena, seniors are probably more easily swayed by reverse mortgage marketing, which is full of rosy thinking misleading claims, and tend to play short shrift to downsides/pitfalls.

According to Consumers Union, there are a couple important implications. First, the guidelines for reverse mortgage should be strengthened with tighter, more balanced language requirements. Second, the counseling session needs to be modified, not only to protect borrowers from unscrupulous lenders, but in some cases, to protect them from their own shortcomings.

When you consider the extraordinary number of people that are already (or will soon be) eligible for reverse mortgages, their $4 trillion in latent home equity, and the financial anxiety affecting senior citizens, you would think that the reverse mortgage business would be booming. While growth over the last decade has been impressive, however, 2010 was a fairly disappointing year, with only 100,000 new reverse mortgages issued. What’s holding the industry back? In one word: culture.

The statistics would certainly seem to suggest that Americans are comfortable with debt. Though this is undoubtedly the case, most borrowers nonetheless look forward to being debt-free. That is especially true when it comes to borrowing for a home, and there is a negative connotation associated with being a mortgage slave. After 30 years (perhaps more if the mortgage was refinanced) and hundreds of thousands of dollars in interest, being debt-free would be cause for celebration (and maybe even a ritual mortgage burning) by even the most stoic homeowners.

To then commit to obtaining a new mortgage might take more than some glossy brochures and a clever sales pitch. Why go through all of the aggravation of borrowing money to purchase a home and dutifully repay that loan, simply to undo all of that work with a fresh loan? After all, there is a certainly a tremendous amount of pride (not to mention security) in owning one’s home – the most fundamental possession – outright.

In addition, people naturally become more conservative as they age, and that is especially true when it comes to finances. Due to its costs and the fact that it represents an obligation, a reverse mortgage entails the assumption of risk. Those that have recently retired or are nearing retirement are not naturally inclined to take risks with their finances. In that sense, the only demographic that is eligible for the reverse mortgage is also perhaps the least likely to take advantage of it.

Finally, more than with any other possession, there is a great sense of personal nostalgia and connection attached to one’s home. Having lived in the same home long enough to repay a mortgage also means that many of one’s major life memories are associated with that home. By obtaining a reverse mortgage, a borrower must accept the strong possibility that the property will one day be sold to repay it. In other words, a reverse mortgage represents a sort of death knell for one’s home.

On the other hand, there may also exist the possibility that the home will need to be sold at some point anyway (either for financial reasons or simply because one’s heirs no longer wish to keep it), which means that this shouldn’t be a factor in obtaining a reverse mortgage. In addition, while there is something to be said for wanting to remain debt-free after repaying one’s primary mortgage, there is still a huge pool of eligible reverse mortgage borrowers that have yet to (or are unable to) repay their primary mortgages, and for whom financial conservatism isn’t realistic.

It is these borrowers that are best suited to obtaining reverse mortgages, and to whom the reverse mortgage industry should be spending the brunt of its time trying to convince.

This is precisely what the Citizens League, an advocacy group based in Minnesota, proposed in their recent report, “Moving Beyond Medicaid: Long-Term Care for the Elderly as a Life Quality and Fiscal Imperative.” If current trends continue, Minnesota’s Medicaid system will be impossible to sustain in its current form, and the solution may involve reverse mortgages.

The report offers some grim statistics about the situation in Minnesota, which can also be seen as a microcosm for a national problem. In sum, “40% of the long-term care expenditures for the elderly in Minnesota in 2004 were financed by Medicaid…Medicaid funding for long-term care for the elderly could grow nearly fivefold in Minnesota, from $1.1 billion in 2010 to $5 billion in 2035.” Assuming that taxpayers balk at financing this entire burden using public funds, an alternative system for financing long-term care (for indigent residents) will nee to be created.

While a handful of potential solutions were laid out, I want to focus on the one that involves reverse mortgages. Basically, the Citizens League has suggested eliminating the home-exemption rule, whereby one’s home is not factored into eligibility for medicaid funds. Under the proposal, recipients of medicaid could be prodded to obtain reverse mortgages instead of or in conjunction with medicaid funds. Of course, the reverse mortgage would have to be redesigned in order to provide an additional level of protection for borrowers and to keep costs at an absolute low. Loan amounts would be small (in order to minimize risk and costs), and the proceeds could only be used for medical and long-term care expenses.

The benefits to state governments would be fantastic: “It has been estimated that replacing Medicaid’s home exemption with “reverse mortgages” could save Medicaid from $5 to $20 billion a year in the United States. When you consider that states are increasingly strapped for cash and that taxpayers are demanding cuts in public programs, this idea is a practicable way to shift some of the medicaid burden onto those that benefit directly from its services.

In a recent TV program and accompanying article, CBS News recently reported on the virtues of the HECM Saver. While CBS was right to praise this latest addition to the HECM reverse mortgage series of products, it praised it for the wrong reasons. Sadly, its news coverage demonstrated a serious lack of understanding of the HECM Saver.

The Home Equity Conversion Mortgage (HECM) Saver was introduced in late 2010 by the FHA in response to criticisms that the existing product, the HECM Standard, was not economical for most borrowers. With the HECM Saver, the expensive upfront mortgage insurance premium was effectively eliminated (though the annual insurance premium was left in place). To compensate for the increased risk and to minimize the chance of default, the FHA also reduced principal limits for the new product.

According to CBS News, you can now save money on interest when you obtain a reverse mortgage. This is wrong on two accounts. First of all, while it’s true that mortgage rates are at record lows, the FHA has mandated an interest rate floor for fixed-rate reverse mortgages at 5%. Second, the HECM Saver often carries a slightly higher rate of interest (for both fixed and variable rates) than its counterpart, the HECM Standard, undoing some of the savings from a lack of upfront insurance premium.

CBS News’ second mistake was to advise borrowers to “Consider the loan to fill short-term needs.” This was predicated on the assumption that other “fees are waived,” but this is hardly a given. In addition, while the lack of upfront insurance premium means that reverse mortgages are cheaper than before, they still carry significant upfront costs, exceeding 5% of the value of the loan. The only way such costs can be rationalized is if the reverse mortgage remains outstanding for many years. When you factor in the annual insurance premiums, service fees, etc., a reverse mortgage will almost always be more expensive than other types of loans. A Home Equity Line of Credit (HELOC), for example, is probably a better choice for borrowers with short-term needs.

Ultimately, the HECM Saver was created not for the benefit of borrowers with short time horizons, but rather for borrowers with smaller capital needs. Those that don’t require massive loans, but otherwise are well suited for the HECM Standard, would be wise to consider it. For all other borrowers, a reverse mortgage of any kind should continue to be thought of as a last resort only.

A recent survey sponsored by the National Reverse Mortgage Lenders Association (NRMLA) suggests that reverse mortgages are the panacea for senior citizens’ financial problems. While there are reasons to be skeptical of the survey (because of who funded it) there are also reasons to stand behind it and ponder its implications.

The poll was conducted on behalf of the NRMLA by Marttila Strategies. It involved 1,800 seniors and their adult children and was titled “The Retirement Abyss: America’s Seniors’ Search for Security.” According to the survey, “one-in-four seniors believe they will not be able to cover their monthly expenses in retirement, such as housing and utilities, and nearly 20 percent believe that, without additional cash flow, they will have to give up their homes.” In addition, a whopping 85% of those polled were pessimistic about the state of the economy, and 50% worry about supporting themselves in retirement. This is supported by current economic data, which show rising poverty rates among the elderly.

The survey also established that 80% of seniors want to keep their homes. This jibes with a similar survey conducted by the Joint Center for Housing Studies of Harvard University, which found that, “95 percent of seniors surveyed over the age of 75 want to remain and age in their home.” This presents an obvious conundrum: seniors want to remain in their homes, but lack the cash to do so.

Enter the reverse mortgage…

According to the survey, “74% of reverse mortgage borrowers in the survey described their use of a reverse mortgage as a positive experience. Seniors in the survey expressed that they understood the financial terms of the product very well (75%) and ninety percent felt no sales pressure as part of the reverse mortgage process.” That would seem to rebut the claims of reverse mortgage critics, who continue to insist that reverse mortgages are poorly understood and inappropriate for most borrowers.

On the other hand, the survey also inadvertently confirmed these criticisms, since more than one quarter of all borrowers was either unhappy with or didn’t adequately understand the product’s financial terms. What this probably means in practice is that many borrowers either failed to properly investigate or simply overlooked the high upfront costs and rapid accrual of interest, until they went to repay their reverse mortgages and/or discovered that their home equity had been vastly depleted. These borrowers would no doubt be unlikely to recommend reverse mortgages to other borrowers.

Nonetheless, while the industry could certainly do more to discourage unsuitable borrowers from obtaining reverse mortgages, it deserves credit for the high rates of satisfaction among existing borrowers. For those that meet certain criteria, reverse mortgages can seem like a windfall. As one borrower summarized, “Why on earth aren’t more people telling seniors about this Federally Insured Reverse Mortgage?”

This is my second post in my coverage of the widely circulated Consumers Union report entitled, “Examining Faulty Foundations in Today’s Reverse Mortgages.” In this post, I want to examine the section “Reverse Mortgage Pitfalls” as part of a broader examination of the risks surrounding reverse mortgages.

The report identifies a handful of specific pitfalls. First, there are suitability concerns; namely, reverse mortgages aren’t appropriate for a significant portion of eligible borrowers. According to Consumers Union, “The right reverse mortgage may be appropriate for some low-income relatively healthy seniors who lack other retirement assets, do not qualify for lower-cost alternatives and cannot meet their current mortgage obligation.” On the other hand, those whose health is questionable and/or have definitive plans to move into an assisted living facility at some point should probably avoid reverse mortgages.

Second, there are concerns over the disbursement of and use of the reverse mortgage proceeds. Some borrowers withdraw the maximum amount of equity because they think they should, rather than leaving it in a line of credit account to accumulate interest. Many borrowers also make the mistake of treating reverse mortgage proceeds as a windfall – when it is really a loan – and spend it on frivolous or lifestyle purchases, rather than on necessary living expenses.

Third, many borrowers fail to fully understand the costs of the reverse mortgage because they are deducted from home equity rather than paid directly by the borrower. Along these lines, they fail to appreciate that upfront costs are substantial, and that combined with the compounded interest on the negatively amortizing loan, their home equity may deplete itself in 10-15 years or less.

Next, some borrowers also fail to realize that a reverse mortgage can affect their eligibility for certain government benefits, such as social security and medicaid. According to Consumers Union, “A ‘lump sum’ reverse mortgage payout will immediately put the elder above the asset limit for SSI/Medicaid and disqualify the senior for these important benefits, unless careful legal planning is done to avoid this result.” Before obtaining a reverse mortgage then, all prospective borrowers should research the impact on the money they expect to receive from government entitlement programs.

Finally, due both to deceptive marketing and an inherent lack of understanding, borrowers fail to grasp that a reverse mortgage is a loan agreement, and violating the terms could result in foreclosure. For example, unlike with a conventional mortgage, reverse mortgages do not require the funding of escrow accounts to pay property taxes, hazard insurance premiums, and for routine home maintenance. It is vital that borrowers understand that neglecting to make these payments (out-of-pocket) could trigger a default on the loan and even foreclosure.

For additional information, I would encourage you to consult the Consumers Union report, and to read a couple related posts that I wrote earlier, here and here.

Consumers Union, the non-profit publisher of the Consumer Reports magazine series, recently released a stinging report entitled, “Examining Faulty Foundations in Today’s Reverse Mortgages.” I will address the report in its entirety in a later post, but for now, I would like to focus exclusively on the section on reverse mortgage alternatives.

The report jibes with the advice that I have proffered on this website, and advises that, “Reverse mortgages are very expensive loans, and as such, they should be considered only as a last resort.” Accordingly, Consumers Union recommends that prospective borrowers “should first determine if he or she qualifies for less expensive programs…including Supplemental Security Income (SSI), Medicaid, prescription drug discount programs, energy and telephone discount programs, City and County grants and low-cost home improvement loans (sometimes called “single purpose” loans), state property tax postponement programs, In-Home Supportive Services, and Veterans pensions to pay for in-home care.” The report includes a reference to HECM Resources, a fantastic website with a comprehensive listing of reverse mortgage alternatives, organized by state.

Consumers Union also devotes considerable space to so-called Family Financing. Just as it sounds, this involves a loan from family members (or friends) to the homeowner in lieu of a reverse mortgage. The advantages of this kind of reverse mortgage are primarily financial. Even if the family member(s) charge a comparable rate of interest on the loan, the absence of insurance premiums, origination fees, service fees, and other closing costs will yield significant cost savings over the life of the mortgage, which means there is more home equity left over if/when the home is ultimately sold. Since the loan lacks insurance, however, there are downside risks. Namely, if the home equity falls below the balance of the the reverse mortgage, the lending family member will have no way to collect the difference. Depending on how this is resolved, this could lead to awkwardness and even resentment.

There are a handful of other alternatives that the report doesn’t explore. Common-sense possibilities include consuming less and saving more, retiring later, and/or downsizing into a smaller home. Prospective borrowers can also cash in life insurance policies or borrow from retirement accounts. More complicated solutions include HELOC loans, single-purpose reverse mortgages, and even products that forgo home appreciation in return for a one-time payment to the homeowner.

For those borrowers that are determined to obtain a reverse mortgage, you should consider that you still have options. There are HECM Saver loans and HECM Standard loans, fixed-rate loans and variable-rate loans, loans that disburse all of the proceeds upfront and loans that make term/tenure payments over the life of the life. The point is simply to understand all alternatives (both aside from and within reverse mortgages) and make an informed decision.

I have already reported at length (“Fed Recommends Enhanced Reverse Mortgage Disclosure“) on the Federal Reserve’s attempt to enhance the regulatory framework governing reverse mortgages. As it turns out, the proposed regulation has been met with protests by consumer groups, and may require some fine-tuning before it becomes law.

“A coalition of consumer advocacy organizations…consisting of the Center for Responsible Lending, the National Consumer Law Center, the National Association of Consumer Advocates, the California Reinvestment Coalition, the National Fair Housing Alliance, Consumers Union, Consumer Action, the Neighborhood Economic Development Advocacy Project and the National Community Reinvestment Coalition,” has attacked a few specific components of the proposed regulation.

The first source of contention is a loophole in the rule that prevents cross-selling of financial products. Under the original proposal, lenders would have been barred from requiring borrowers to purchase additional financial products (namely annuities and life insurance policies). However, the guideline has since been revised to allow cross-selling, as long as it takes place more than 10 days after the loan is closed. While this would theoretically still make cross-selling difficult, in practice it could easily be circumvented.

The second problem was a change in the Right of Rescission rule, which gives borrowers the right to cancel their reverse mortgage for any reason within 3 days of obtaining it, and to restructure/refinance a reverse mortgage within 3 years if it was determined that the lender misrepresented the costs. Under the revised rules, the 3-year Right of Rescission would be either eliminated altogether, or the language would simply be altered to make it more difficult for borrowers to exercise this right. The result, argues the Coalition, is that lenders will be disinclined towards accuracy when selling reverse mortgages.

Finally, the Consumer Financial Protection Bureau, which was recently created and vested with the power to study and regulate reverse mortgages (among other things) would see its power and influence vastly eroded by the Federal Reserve’s proposed guidelines. As a result, the Federal Reserve Board would be the only quasi-government body keeping watch over the industry.

There are a handful of other criticisms and suggestions which were put forward during the 90-day comment window. (You can view them in their entirety here). The Fed now has an indeterminate period of time to review these comments and make further revisions.

I’m monitoring the situation closely and will try to provide regular updates.

According to a recent survey by LendingTree.com, the majority of borrowers do not shop around before obtaining a mortgage. Given that a reverse mortgage is a standardized product, insured by the FHA and regulated by the Federal Reserve – reverse mortgage borrowers can be excused for having the same mentality. Ultimately, this is a big mistake, and prospective borrowers would be wise to query a few lenders before obtaining a reverse mortgage.

In terms of selecting an HECM lender, you should begin by asking friends and families for referrals, and or contacting any brokers or loan officers with whom you already have a relationship. [(For the minority of borrowers that plan to obtain a proprietary (i.e. jumbo) reverse mortgage, bear in mind that the number of lenders is quite small].If this is not an option, you can use our Reverse Mortgage lender listing, which is organized by state. You should also consult the lender database of the National Reverse Mortgage Lenders Association (NRMLA), the main industry association, whose members include almost all reputable reverse mortgage lenders. Finally, you can search the Federal Department of Housing and Urban Development (HUD) database of HECM lenders. You should only deal with those lenders that have state licensing and are approved by the FHA.

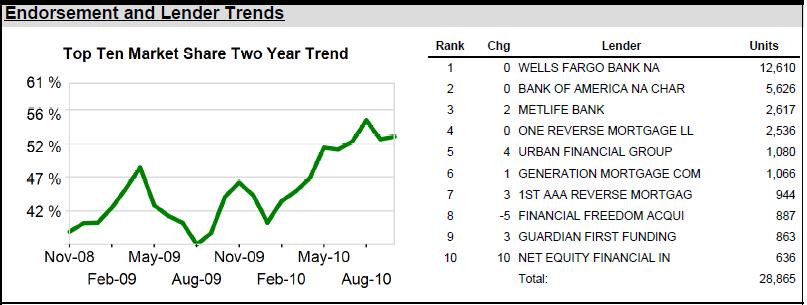

The first major decision is whether you want to deal with a large (national) lender or a small, community lender. In theory, all reverse mortgage lenders offer an identical loan, but the level of service and some of the fees can differ meaningfully from lender to lender. The benefit of dealing with a smaller lender is that you may be able to establish a closer relationship with your loan officer, whereas a national lender might be able to offer you the best deal. According to Reverse Mortgage Insight, Wells Fargo and Bank of America are the two dominant lenders, and the Top Ten Lenders are increasing their dominance of reverse mortgage lending.

At this point, you can start to make contact with specific lenders. Fortunately, reverse mortgage lenders have no reason to pull your credit report, and your credit will not suffer from obtaining quotes from multiple lenders. You should confirm that your lender is willing to offer you the lowest available fixed interest rate (currently set at 5% by the FHA) or a low margin in the case of a variable rate reverse mortgage (~2.25% for HECM Standard and ~2.75% for HECM Saver). Next, you should verify the lender’s fees and other closing costs, and ask if they can waive any fees and/or provide a discount.

Next, you should ask each lender for an explanation of the risks associated with your reverse mortgage as well as any recommended alternatives. If you are already well-informed, you probably won’t learn anything new from this kind of inquiry. Rather, it represents a rudimentary method for gauging the the honesty of your lender. If he pays short shrift to the risks and alternatives, it might be signal that he is incentivized to sell you a reverse mortgage, and any advice he offers is therefore dubious. Along the same lines, you should confirm that you will not be required to purchase other financial products (such as an annuity) in conjunction with your reverse mortgage. This practice is extremely disreputable and often illegal!

After comparing fees, rates, and service, you are ready to make a decision. Don’t feel pressured to choose a specific lender, for whatever reason. And remember that if after obtaining a reverse mortgage you suddenly have regrets, you have 72 hours to exercise your Right of Rescission. In this case, you can either start from scratch with a different lender, or simply forgo obtaining a reverse mortgage altogether.